Financial Capital Remains Hurdle for Women Entrepreneurs

/“Data reveal that an increasing number of women are choosing entrepreneurship as a career path, and of those, a growing number of them share aspirations for growth.” That fact, pointed out in the preface of a new book co-written by a local university professor, is the proverbial tip of the iceberg. According to the U.S. Census Bureau, there are roughly 9.9 million women-owned firms in the United States, representing over a third of all firms in the country—and the ranks of new enterprises with women at the helm are growing rapidly. Between 2007 and 2012, women-owned firms in the U.S. grew by 27 percent compared to a growth rate of 2 percent for firms overall.

“But in spite of their impressive growth in numbers,” writes University of Hartford finance professor Susan Coleman, “the business ventures women are launching today continue to lag behind those launched by men in terms of revenues and employment. So while an increasing number of women can count themselves as entrepreneurs, many appear to be running into barriers, as the vast majority of their businesses remain quite small.”

Coleman, along with Alicia M. Robb, have co-authored The Next Wav e: Financing Women’s Growth-Oriented Firms (published by Stanford University Press), which points to “three essential factors that women entrepreneurs need to thrive: knowledge, networks, and investors. In tandem, these three ingredients connect and empower emerging entrepreneurs with those who have succeeded in growing their firms while also realizing the financial and economic returns that come with doing so.”

e: Financing Women’s Growth-Oriented Firms (published by Stanford University Press), which points to “three essential factors that women entrepreneurs need to thrive: knowledge, networks, and investors. In tandem, these three ingredients connect and empower emerging entrepreneurs with those who have succeeded in growing their firms while also realizing the financial and economic returns that come with doing so.”

Robb is Senior Fellow with the Ewing Marion Kauffman Foundation and Visiting Scholar at the University of California, Berkeley and the University of Colorado, Boulder. She previously worked with the Office of Economic Research in the Small Business Administration and the Federal Reserve Board of Governors. Coleman is Professor of Finance and Ansley Chair at the Barney School of Business at the University of Hartford.

Coleman notes that “A crucial pitfall is that women face unique challenges in their attempts to acquire financial capital. Growth-oriented firms typically require substantial investment—both in the form of bank loans and external equity in the form of angel or venture capital funding—to scale up.” Studies reveal, however, that “women entrepreneurs raise significantly smaller amounts of capital than men and face continued barriers in their attempts to secure external equity in particular,” Coleman points out.

In the book’s forward, the authors explain that the motives behind women-run entrepreneurial businesses vary. “Some of these growth-oriented entrepreneurs are motivated by a desire to pursue an opportunity or an unmet need in the marketplace. Others are frustrated by the constraints imposed by a ‘glass ceiling’ that prevents them from reaching the most senior ranks of corporations. Still others are drawn by the financial and economic rewards that can come from leading a firm that achieves scale.”

According to IRS data, women represent over 40 percent of top wealth holders in the United States, yet estimates from the University of New Hampshire’s Center for Venture Research indicate that they represented only 25 percent of angel investors in 2015, Coleman notes.

Optimistic about the future success of women entrepreneurs, Coleman and Robb observe that “Successful women entrepreneurs who are paying it forward in a variety of ways are a driving force” in what they describe as the “next wave.”

“In a virtuous cycle, women entrepreneurs evolve from being the recipients of human, social, and financial capital into becoming the providers of those key resources as their firms grow and create economic value. The more successful women at the helm of businesses that kick off cash, the more women there are to invest in others, and the faster we see the number of women grow in the ranks of larger businesses and investing.”

In addition to appreciation expressed to the Kansas City-based Kauffman Foundation for financial support, the book’s acknowledgements note that the Barney School of Business and the University of Hartford’s Women’s Education and Leadership Fund provided grants that helped support initial research and development of case studies on women entrepreneurs. The authors also expressed appreciation to three University of Hartford graduate assistants – Ece Karhan, Mert Karhan, and Isha Sen – who “played an invaluable role in the book’s development.”

suranceQuotes, found that the average increase in premiums across the country when a teen driver is added to an existing policy is 79 percent. That is a slight improvement from a few years ago, when the increase nationwide averaged 84 percent.

suranceQuotes, found that the average increase in premiums across the country when a teen driver is added to an existing policy is 79 percent. That is a slight improvement from a few years ago, when the increase nationwide averaged 84 percent.

Perhaps the most significant underlying factor is that each state regulates insurance differently, and those regulatory differences account for some of the variations in the study’s findings, according to insuranceQuotes. For instance, Hawaii is the only state that doesn't allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means that the cost for teens doesn't differ much from the cost for adults buying auto insurance. This may also account for lower increases in states such as New York, Michigan and North Carolina, where insurance is regulated more strictly and rating factors are more stringent, insuranceQuotes points out. The increases in those states when adding a teen to an existing policy were all below 60 percent, among the lowest increases in the nation.

Perhaps the most significant underlying factor is that each state regulates insurance differently, and those regulatory differences account for some of the variations in the study’s findings, according to insuranceQuotes. For instance, Hawaii is the only state that doesn't allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means that the cost for teens doesn't differ much from the cost for adults buying auto insurance. This may also account for lower increases in states such as New York, Michigan and North Carolina, where insurance is regulated more strictly and rating factors are more stringent, insuranceQuotes points out. The increases in those states when adding a teen to an existing policy were all below 60 percent, among the lowest increases in the nation.

The analysis points out that the type of land in a given area has a significant impact on its worth. Agricultural and other largely undeveloped areas are generally worth significantly less than cities and suburbs land. Developed land, or land where housing, roads, and other structures are located, is valued at an estimated $106,000 per acre, while undeveloped land was estimated at $6,500 per acre, and farmland at only $2,000 per acre, according to the analysis.

The analysis points out that the type of land in a given area has a significant impact on its worth. Agricultural and other largely undeveloped areas are generally worth significantly less than cities and suburbs land. Developed land, or land where housing, roads, and other structures are located, is valued at an estimated $106,000 per acre, while undeveloped land was estimated at $6,500 per acre, and farmland at only $2,000 per acre, according to the analysis.

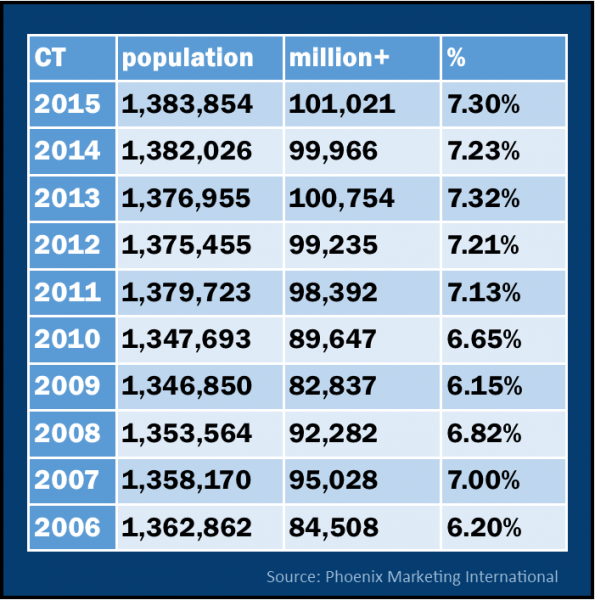

The Latino and Puerto Rican Affairs Commission (LPRAC) was created by an act of the Connecticut General Assembly (CGA) in 1994. This 21 member non-partisan commission is mandated to make recommendations to the CGA and the Governor for new or enhanced policies that will foster progress in achieving health, safety, educational success, economic self-sufficiency, and end discrimination in Connecticut. As of 2014, the state’s Hispanic population exceeded 500,000, about 15 percent of the state’s overall population.

The Latino and Puerto Rican Affairs Commission (LPRAC) was created by an act of the Connecticut General Assembly (CGA) in 1994. This 21 member non-partisan commission is mandated to make recommendations to the CGA and the Governor for new or enhanced policies that will foster progress in achieving health, safety, educational success, economic self-sufficiency, and end discrimination in Connecticut. As of 2014, the state’s Hispanic population exceeded 500,000, about 15 percent of the state’s overall population. ”

”

In addition to the public poll,

In addition to the public poll,

He added, “We advised him that there are ways to be close to family and friends in Connecticut on occasion that are perfectly legal. We're trying to send a more welcoming message to the high earners as a group." Homeowners who spend more than 183 days in the state are considered residents for tax purposes.

He added, “We advised him that there are ways to be close to family and friends in Connecticut on occasion that are perfectly legal. We're trying to send a more welcoming message to the high earners as a group." Homeowners who spend more than 183 days in the state are considered residents for tax purposes. wealthiest individuals, had relocated from Greenwich to Florida, the second individual in that tax bracket to do so recently. The exits, the Courant reported, “leave Connecticut with 13 billionaires, including Ray Dalio ($15.6 billion) and Steven Cohen ($12.7 billion), both hedge fund owners who live in Greenwich.” Eight of those 13 state residents list Greenwich as their home address, according to

wealthiest individuals, had relocated from Greenwich to Florida, the second individual in that tax bracket to do so recently. The exits, the Courant reported, “leave Connecticut with 13 billionaires, including Ray Dalio ($15.6 billion) and Steven Cohen ($12.7 billion), both hedge fund owners who live in Greenwich.” Eight of those 13 state residents list Greenwich as their home address, according to

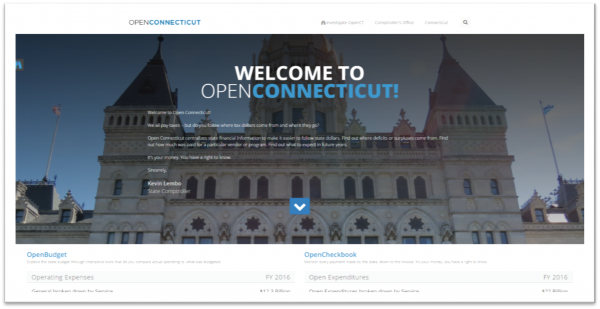

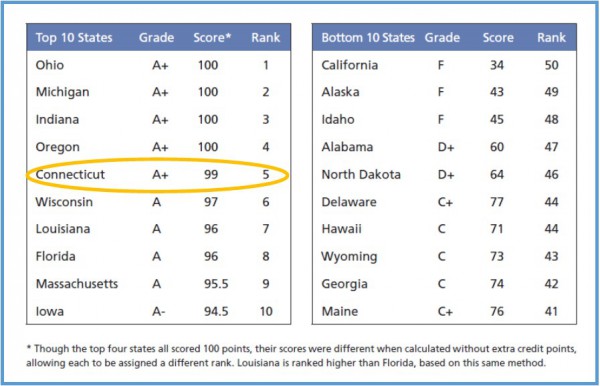

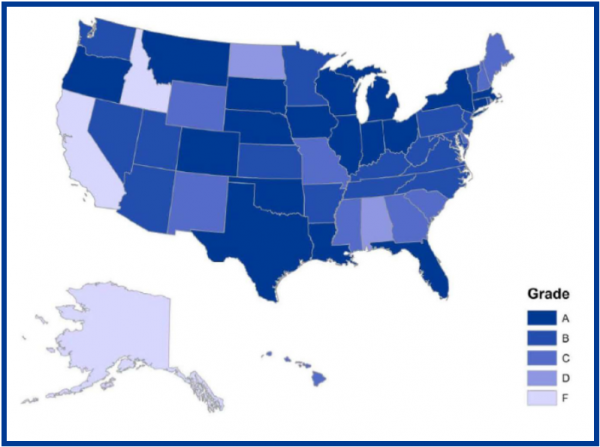

Based on an inventory of the content and ease-of-use of states' transparency websites, the report assigns each state a grade of “A+” to “F.” The leading states with the most comprehensive transparency websites are Ohio, Michigan, Indiana, Oregon, and Connecticut, with each receiving an A+ grade.

Based on an inventory of the content and ease-of-use of states' transparency websites, the report assigns each state a grade of “A+” to “F.” The leading states with the most comprehensive transparency websites are Ohio, Michigan, Indiana, Oregon, and Connecticut, with each receiving an A+ grade.

inue to improve, the states that most distinguished themselves as leaders in spending transparency are those that provide access to types of expenditures that otherwise receive little public scrutiny. Only 11 states- including Connecticut - provide checkbook-level information that includes the recipients of each of the state’s most important subsidy programs.

inue to improve, the states that most distinguished themselves as leaders in spending transparency are those that provide access to types of expenditures that otherwise receive little public scrutiny. Only 11 states- including Connecticut - provide checkbook-level information that includes the recipients of each of the state’s most important subsidy programs.

In an article appearing in this week’s

In an article appearing in this week’s