CT is Among 24 States Seeing Weak Revenues, Highest Number Since Recession

/Connecticut is not alone. According to the National Association of State Budget Officers’ (NASBO) annual state spending survey, half of all states saw revenues come in lower than budgeted in fiscal 2016 and 24 states – including Connecticut - are seeing those weak revenue conditions carry into fiscal 2017.

That is the highest number of states falling short of revenue projections since 36 states budgets missed their mark in 2010, according to the NASBO report and Governing. As a result, 19 states made mid-year budget cuts in 2016, totaling $2.8 billion, Connecticut among them. That number of states “is historically high outside of a recessionary period,” according to the report. The revenue slowdown is caused mainly by slow income tax growth, even slower sales tax growth and an outright decline in corporate tax revenue, the report explains, stating that “progress since the Great Recession has been uneven, and many states are seeing softening state tax collections.”

That is the highest number of states falling short of revenue projections since 36 states budgets missed their mark in 2010, according to the NASBO report and Governing. As a result, 19 states made mid-year budget cuts in 2016, totaling $2.8 billion, Connecticut among them. That number of states “is historically high outside of a recessionary period,” according to the report. The revenue slowdown is caused mainly by slow income tax growth, even slower sales tax growth and an outright decline in corporate tax revenue, the report explains, stating that “progress since the Great Recession has been uneven, and many states are seeing softening state tax collections.”

Overall, state spending totaled $786 billion last fiscal year, a 3.7 percent annual increase. Although it marks the seventh straight year of spending growth, it represents a slowdown from fiscal 2015 when spending increased by 4.4 percent.

“Weaker-than-anticipated revenue collections and resulting budget gaps in fiscal 2016 led some states to cut spending during the year,” the report indicated, with overall spending increasing just 1.8 percent to $781 billion in fiscal 2016, compared with the previous year’s growth of 5 percent. When accounting for inflation, 32 states are still spending less than they did before the Great Recession and total state spending also has yet to surpass pre-recession levels. Across the states, cuts enacted by legislatures come most often in K-12 education, an “all other” category, followed by Medicaid, higher education and corrections, according to data compiled for the NASBO report.

The state has an estimated $1.3 billion or $1.5 billion budget deficit, according to reports from the governor’s Office of Policy and Management and the legislature’s nonpartisan Office of Fiscal Analysis, CTNewsJunkie reported recently.

“Certainly a recession is coming sometime soon,” said NASBO President-elect Michael Cohen, who is also California’s finance director, told Governing. “But I think economists in all of the state offices would tell you that’s a really hard economic forecasting [task] of predicting when that’s going to happen.” NASBO had previously predicted that fiscal 2016 would mark the full recovery of state budgets from the recession, but the cutbacks and increased inflation has delayed that at least another year.

The report indicates that eight (including energy-producing states like Alaska, North Dakota and Oklahoma) planned to spend less in 2017, and 11 states planned to up their spending by 6 percent or more next year. In those states, sales tax increases have improved their revenue with Louisiana, for example, anticipating a 17 percent increase in revenue, driven by an expected $800 million increase in sales tax collections.

Most states have focused on strengthening their rainy day funds, according to the report, though some states – particularly energy-producing ones – have had to tap their reserves to help address budget shortfalls. Twenty-nine states increased their rainy day fund balances in fiscal 2016, and 25 states project increases in fiscal 2017. Since aggregate rainy day fund levels hit a recent low in fiscal 2010, 40 states had increased their amounts as of the end of fiscal 2016, at least in nominal terms, the report said.

“States will also have to contend with rising spending demands in areas such as health care and education, long-term pressures such as pensions and infrastructure, and increasing federal uncertainty,” the report predicted, “particularly concerning the prospects of tax reform and health care policy. In this environment, states are likely to be cautious in their spending and revenue forecasts, as they continue to focus on ensuring structurally balanced budgets.”

https://youtu.be/uAvz-zo9NQw

Louise DiCocco, Assistant Counsel for the Connecticut Business & Industry Association, noted that “24 years ago, more than 80 percent of Connecticut votes overwhelmingly approved a spending cap to keep the cost of state government within the taxpayers’ means to afford it. Voters demanded the cap as an offset to the persona income tax in Connecticut. The state must enact a spending cap that is ironclad and works.”

Louise DiCocco, Assistant Counsel for the Connecticut Business & Industry Association, noted that “24 years ago, more than 80 percent of Connecticut votes overwhelmingly approved a spending cap to keep the cost of state government within the taxpayers’ means to afford it. Voters demanded the cap as an offset to the persona income tax in Connecticut. The state must enact a spending cap that is ironclad and works.”

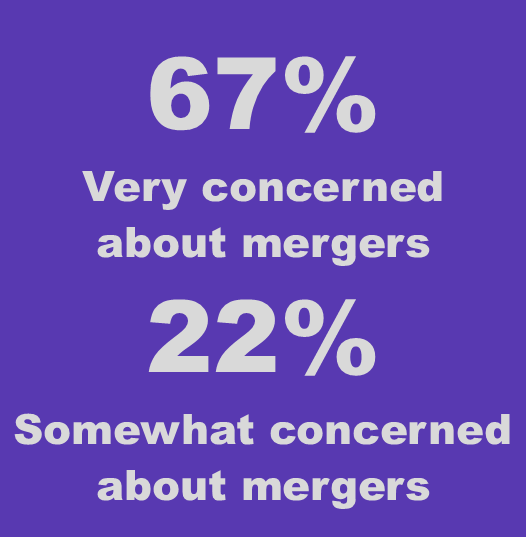

In recent months, First Niagara did consolidate five Connecticut branches (Woodstock, Dayville, Hamden, East Haven and Madison), and all of the employees who worked at those branches were offered positions within the bank, officials indicated, and no layoffs were associated with that consolidation.

In recent months, First Niagara did consolidate five Connecticut branches (Woodstock, Dayville, Hamden, East Haven and Madison), and all of the employees who worked at those branches were offered positions within the bank, officials indicated, and no layoffs were associated with that consolidation.

At #296 is Glastonbury-based Fiondella Milone & LaSaracina. FML was founded in 2002 “for the purpose of providing professional auditing, tax and business consulting services to a wide range of clients and industries throughout the Northeast,” the company’s website indicates. After working together at Ernst & Young, the firm’s founding partners, Jeff Fiondella, Frank Milone and Lisa LaSaracina launched FML.

At #296 is Glastonbury-based Fiondella Milone & LaSaracina. FML was founded in 2002 “for the purpose of providing professional auditing, tax and business consulting services to a wide range of clients and industries throughout the Northeast,” the company’s website indicates. After working together at Ernst & Young, the firm’s founding partners, Jeff Fiondella, Frank Milone and Lisa LaSaracina launched FML. counting newsletter and the award-winning National Benchmarking Report.

counting newsletter and the award-winning National Benchmarking Report.

e: Financing Women’s Growth-Oriented Firms (published by Stanford University Press), which points to “three essential factors that women entrepreneurs need to thrive: knowledge, networks, and investors. In tandem, these three ingredients connect and empower emerging entrepreneurs with those who have succeeded in growing their firms while also realizing the financial and economic returns that come with doing so.”

e: Financing Women’s Growth-Oriented Firms (published by Stanford University Press), which points to “three essential factors that women entrepreneurs need to thrive: knowledge, networks, and investors. In tandem, these three ingredients connect and empower emerging entrepreneurs with those who have succeeded in growing their firms while also realizing the financial and economic returns that come with doing so.”

suranceQuotes, found that the average increase in premiums across the country when a teen driver is added to an existing policy is 79 percent. That is a slight improvement from a few years ago, when the increase nationwide averaged 84 percent.

suranceQuotes, found that the average increase in premiums across the country when a teen driver is added to an existing policy is 79 percent. That is a slight improvement from a few years ago, when the increase nationwide averaged 84 percent.

Perhaps the most significant underlying factor is that each state regulates insurance differently, and those regulatory differences account for some of the variations in the study’s findings, according to insuranceQuotes. For instance, Hawaii is the only state that doesn't allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means that the cost for teens doesn't differ much from the cost for adults buying auto insurance. This may also account for lower increases in states such as New York, Michigan and North Carolina, where insurance is regulated more strictly and rating factors are more stringent, insuranceQuotes points out. The increases in those states when adding a teen to an existing policy were all below 60 percent, among the lowest increases in the nation.

Perhaps the most significant underlying factor is that each state regulates insurance differently, and those regulatory differences account for some of the variations in the study’s findings, according to insuranceQuotes. For instance, Hawaii is the only state that doesn't allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means that the cost for teens doesn't differ much from the cost for adults buying auto insurance. This may also account for lower increases in states such as New York, Michigan and North Carolina, where insurance is regulated more strictly and rating factors are more stringent, insuranceQuotes points out. The increases in those states when adding a teen to an existing policy were all below 60 percent, among the lowest increases in the nation.

The analysis points out that the type of land in a given area has a significant impact on its worth. Agricultural and other largely undeveloped areas are generally worth significantly less than cities and suburbs land. Developed land, or land where housing, roads, and other structures are located, is valued at an estimated $106,000 per acre, while undeveloped land was estimated at $6,500 per acre, and farmland at only $2,000 per acre, according to the analysis.

The analysis points out that the type of land in a given area has a significant impact on its worth. Agricultural and other largely undeveloped areas are generally worth significantly less than cities and suburbs land. Developed land, or land where housing, roads, and other structures are located, is valued at an estimated $106,000 per acre, while undeveloped land was estimated at $6,500 per acre, and farmland at only $2,000 per acre, according to the analysis.

The Latino and Puerto Rican Affairs Commission (LPRAC) was created by an act of the Connecticut General Assembly (CGA) in 1994. This 21 member non-partisan commission is mandated to make recommendations to the CGA and the Governor for new or enhanced policies that will foster progress in achieving health, safety, educational success, economic self-sufficiency, and end discrimination in Connecticut. As of 2014, the state’s Hispanic population exceeded 500,000, about 15 percent of the state’s overall population.

The Latino and Puerto Rican Affairs Commission (LPRAC) was created by an act of the Connecticut General Assembly (CGA) in 1994. This 21 member non-partisan commission is mandated to make recommendations to the CGA and the Governor for new or enhanced policies that will foster progress in achieving health, safety, educational success, economic self-sufficiency, and end discrimination in Connecticut. As of 2014, the state’s Hispanic population exceeded 500,000, about 15 percent of the state’s overall population. ”

”

In addition to the public poll,

In addition to the public poll,