Millennials Present New Challenges to Insurance Industry Seeking Customers

/Just as recently appointed Connecticut Insurance Commissioner Katharine L. Wade settles in to her job, the insurance industry is facing new challenges from a new generation. A former Cigna executive, Commissioner Wade has more than 20 years of industry experience and oversees a regulatory agency with jurisdiction over one of the largest insurance industries in the United States. Hartford has long been considered the nation’s Insurance Capitol, so changes in the industry reverberate across the Constitution State.

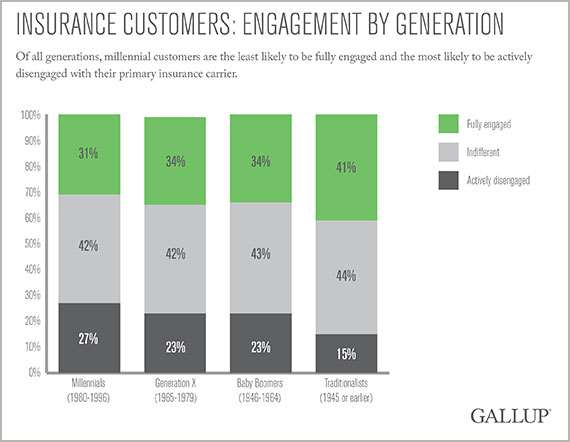

It seems insurance companies have their work cut out for them when it comes to engaging their millennial customers. Of all the generations, millennials (born in 1980 to 1996) are the least likely to be fully engaged -- and the most likely to be actively disengaged -- with their primary insurer, according to a recent Gallup survey.

Millennials are the largest generation in the U.S. and will grow to dominate the market in the years to come, Gallup points out, adding that “insurance executives who neglect to take steps to engage this age group do so at their own peril.”

Millennials are the largest generation in the U.S. and will grow to dominate the market in the years to come, Gallup points out, adding that “insurance executives who neglect to take steps to engage this age group do so at their own peril.”

Insurance companies see substantial business gains when they engage customers of any generation, Gallup finds. Compared with their actively disengaged counterparts, engaged insurance customers are less sensitive about pricing when selecting and retaining a primary insurance carrier. They spend more and buy a wider variety of products, including financial offerings, from their insurer than do actively disengaged customers. They also stay with the company longer and are more likely to recommend it to others.

But building and maintaining customer engagement can be challenging -- especially for insurance companies with a diverse customer base. To raise millennials' engagement -- and thereby ensure a more engaged customer base in the future -- Gallup indicates that "leaders must understand how these young customers differ from others in their engagement and consumer behavior." And they do differ, in substantial ways.

In its 2014 Insurance Panel study, Gallup uncovered insights into what drives millennials to start a relationship or stay in one with an insurance company. The analysis revealed many similarities across generations, but it also uncovered two important approaches to build relationships with millennials, and key factors that differ with past generations.

- Family is key. Millennials are significantly more likely than other generations to have insurance coverage under a family member who chose the company. When their family members value an insurance company's brand, millennials follow suit. This finding contrasts sharply with older generations' prioritization of factors such as cost and company reputation.

- Millennials are more likely to buy insurance online. Millennials are more than twice as likely (27% vs. 11%, respectively) as all other generations to purchase their policies online rather than through an agent. Online purchasing is far from the mainstream among insurance consumers overall -- 74% originally purchased with an agent vs. 14% online -- but if this trend among millennials continues to grow, it could substantially change the way insurance companies interact with customers in the coming years.

The bad news? Millennials are least satisfied of any generation with the online experience, which could contribute to their generally low engagement overall with their primary insurer. Improving interactions with customers online is, therefore, a smart investment toward building strong relationships within this future mainstream customer base, Gallup points out.

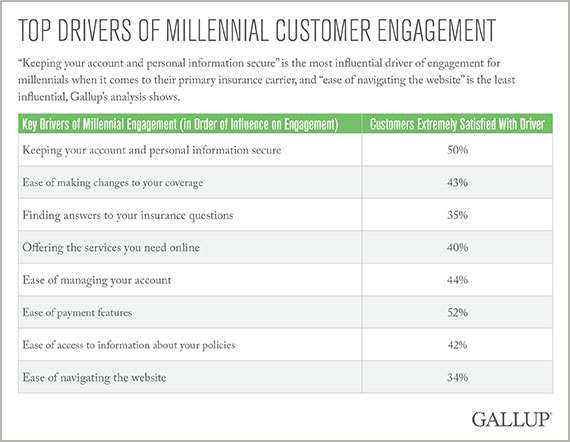

As insurance companies consider ways to improve those relationships with millennial customers, Gallup suggests seven key areas worthy of attention: information security, family incentives, specialized services, ease of making changes to coverage online, ease of finding answers online, easy access to a range of online services, and overall ease of use in areas including account management, payment and website navigation.

Millennials’ distinctive attitudes also extend to car insurance and long-term care insurance, according to other recent surveys.

Cars are increasingly being rejected by many millennials in favor of public transit or other modes of transportation, including increasingly popular ride-for-hire services. As a consequence, car insurance is taking a backseat among some, the website NerdWallet reported this month.  According to a study by the U.S. Public Interest Research Group, Americans are driving fewer total miles today than eight years ago, and driving fewer miles per person than we did in 1996. It is a reversal after decades of steady growth.

According to a study by the U.S. Public Interest Research Group, Americans are driving fewer total miles today than eight years ago, and driving fewer miles per person than we did in 1996. It is a reversal after decades of steady growth.

Millennials are less likely to drive — or even have a driver’s license — than previous generations. From 1983 to 2008, the percentage of Americans age 20 to 24 with a driver’s license fell from about 90 percent of that age group to ju st over 80 percent, according to a University of Michigan study, the website noted. If you don’t own a car, you don’t need car insurance.

st over 80 percent, according to a University of Michigan study, the website noted. If you don’t own a car, you don’t need car insurance.

In addition, Forbes recently reported that many of the nation’s millennials think their boomer parents are doing a lousy job planning for their long-term care needs, according to a survey from Genworth Financial, a leading seller of long-term care insurance policies.

The Aging Across Generations study, conducted with the J&K Solutions research firm, found that 27 percent of millennials would give their parents or loved ones a “failing grade” due to not planning for, or talking about, their long-term care needs. And the kids say they’ll do better, with more than half (56 percent) of millennials surveyed expressing the view that they will plan for their long-term care needs more effectively than previous generations.

Time will tell. Other impacts on the industry are likely to be more noticeable more quickly.