Clueless: Many College Students Don’t Understand How Much Debt They’re Accumulating

/With much public attention focused on the increasing costs of college education and the ever-growing levels of student loan debt saddling graduates of higher education institutions, recent research into what students understand – or don’t understand - about their debt is raising some concern.

A significant share of undergraduate college students, it turns out, do not realize how much they are paying for college or how much debt they are taking on to do so. That is the conclusion of a study of college students’ awareness of their level of debt as they accumulate various loans to pay for their higher education.

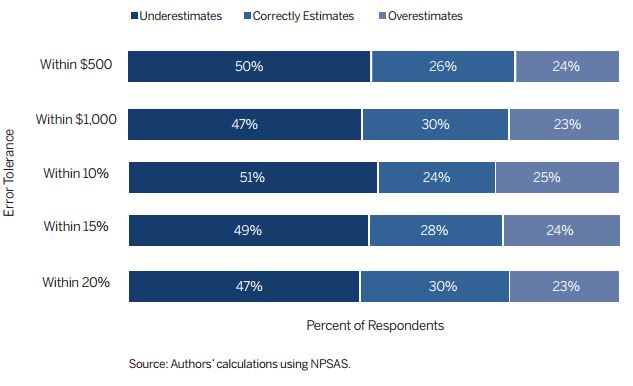

The report, by Brookings Institution, found that “about half of all first-year students in the U.S. seriously underestimate how much student debt they have, and less than one-third provide an accurate estimate within a reasonable margin of error.”

The report, by Brookings Institution, found that “about half of all first-year students in the U.S. seriously underestimate how much student debt they have, and less than one-third provide an accurate estimate within a reasonable margin of error.”

Surprisingly, among students with federal loans, 28 percent reported having no federal debt and 14 percent said they didn’t have any student debt at all, the researchers found. “Enrolled college students,” the report says, “do not have a firm grasp on their financial positions, including both the price they are paying for matriculation and the debt they are accruing.”

Improving the college search process by making college costs more transparent to potential students and their families has been a primary focus of recent higher education policy efforts, the Brookings report points out. “But the importance of this information does not end at the university gates,” the report states.

In the analysis, study authors Elizabeth Akers and Matthew Chingos of the Brown Center on Education Policy at Brookings find that:

- Only a bare majority of respondents (52 percent) at a selective public university were able to correctly identify (within a $5,000 range) what they paid for their first year of college. The remaining students underestimate (25 percent), overestimate (17 percent), or say they don't know (seven percent).

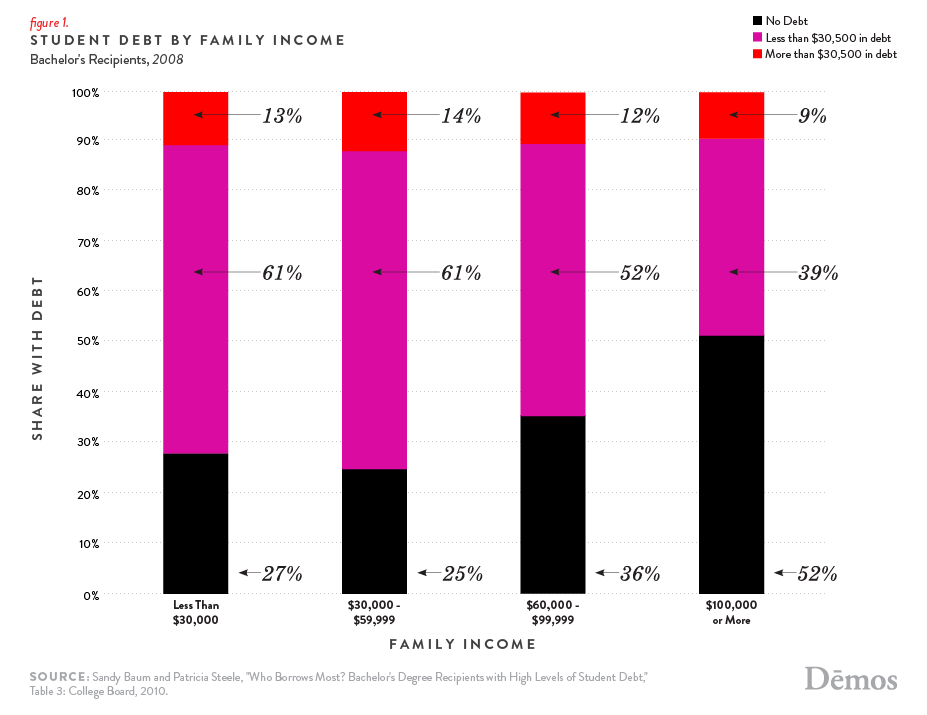

- About half of all first-year students in the U.S. (based on nationally representative data) seriously underestimate how much student debt they have, and less than one-third provide an accurate estimate within a reasonable margin of error. The remaining quarter of students overestimate their level of federal debt.

- Among all first-year students with federal loans, 28 percent reported having no federal debt and 14 percent said they didn’t have any student debt at all.

The report suggests that without a solid understanding of the financial situation, “it’s unlikely that students will be able to make savvy decisions regarding enrollment, major selection, persistence, and employment. Without knowledge of their financial circumstances, a student with a large sum of debt might be unprepared to compete for the jobs that would pay generously enough to allow them to repay their debt without having to enter an income-based repayment program.”

The report also concludes by noting that “many students look back on their educational experiences with some regret about the financial circumstances. Some wish they had not gone to college in the first place, while others wish they had borrowed less or earned a different degree. The lack of literacy about the personal finances of college going is almost certainly leading some students into decisions that they later come to regret. The problem with the lack of financial savvy among enrolled college students is that the consequences of their decisions come as a surprise to them once it’s too late.”

The report also concludes by noting that “many students look back on their educational experiences with some regret about the financial circumstances. Some wish they had not gone to college in the first place, while others wish they had borrowed less or earned a different degree. The lack of literacy about the personal finances of college going is almost certainly leading some students into decisions that they later come to regret. The problem with the lack of financial savvy among enrolled college students is that the consequences of their decisions come as a surprise to them once it’s too late.”

The Brookings Institution is a private nonprofit organization devoted to independent research and innovative policy solutions. The mission of the Brown Center on Education Policy at Brookings is to bring rigorous empirical analysis to bear on education policy in the United States. The primary activities of the Brown Center are based on quantitative social science, and are responsive to the immediate interests and needs of those who participate in policymaking.