Student Debt Nationwide Shows Geographic, Income, Racial Divisions; CT in Debt-High Northeast

/

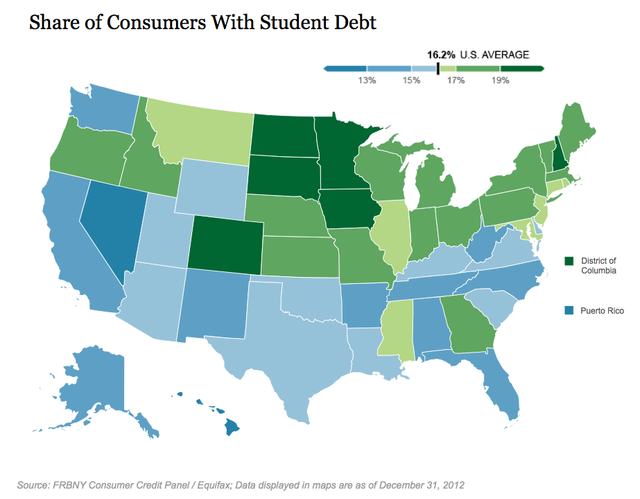

Across the country, an average 16.2 percent of consumers owe some amount of student debt. But if you look at the state level, the country appears split along the Mason–Dixon line, with a higher percentage of the population owing money in northern states than southern states, according to numbers published by the College Financing Group, citing data from the Federal Reserve Bank of New York.

Overall, Hawaii has the lowest share of consumers with student debt, just 12 percent. That’s less than half the rate in Washington, D.C., where 25 percent of the population in Washington, D.C. owes student loan money, according to data compiled through 2012. Connecticut’s rate hovers in the middle, within range of the national average.

According to the Federal Reserve Bank of New York, student loan debt is the only form of consumer debt that has grown since the peak of consumer debt in 2008. Balances of student loans have eclipsed both auto loans and credit cards, making student loan debt the largest form of consumer debt outside of mortgages.

The full report also shows that 11.9% of all borrowers are 90 days or more past due on their loans, and the average student debt per borrower stands at $24,810. Interestingly, despite Washington D.C.’s high percentage of people with student loans, it has a lower-than-average delinquency rate of only 7.3%.

In its most recently updated 2013 quarterly report, the Federal Reserve Bank of New York noted that outstanding student loan balances increased to $994 billion nationwide as of June 30, 2013, a $8 billion increase from the first quarter this year. Other estimates have placed outstanding student debt in excess of $1 trillion.

Life on Hold, Especially Among Lower Income Families

According to a 2012 online web survey conducted by American Consumer Credit Counseling, over 35 percent of respondents reported that they have had to delay saving for retirement because of their student debt, while 27 percent also reported that their ability to buy a car has been impacted, and 29 percent said it has affected their ability to buy a house. Nine percent of respondents said student loan debt has even impacted their ability to get married.

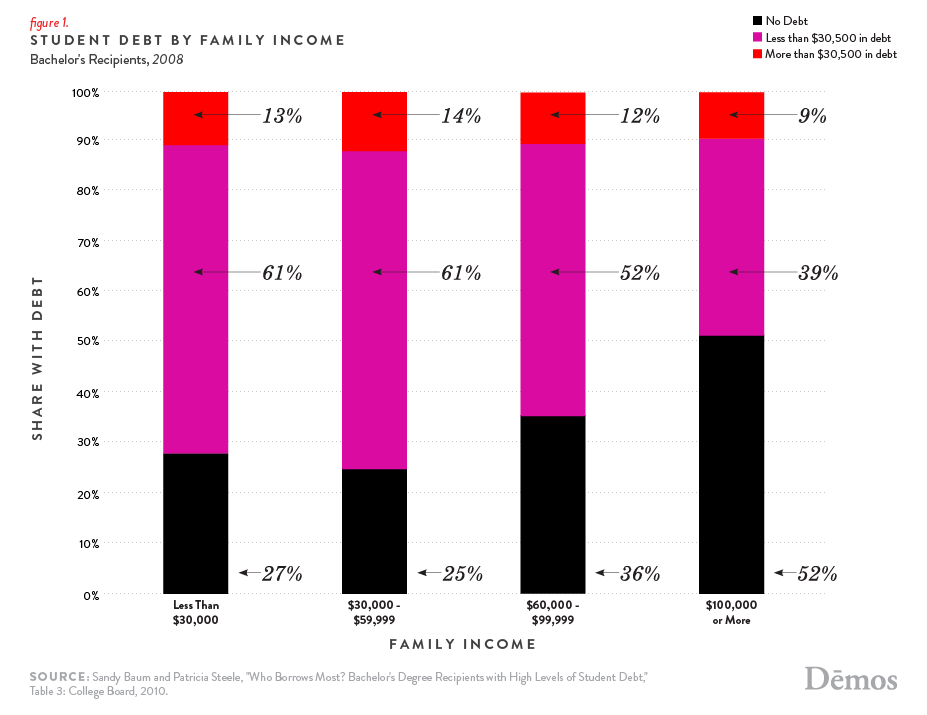

A report this year from Demos, “At What Cost: How Student Debt Reduces Lifetime Wealth,” stated that “though a college education remains the surest path to a middle-class life, evidence has begun to mount that student debt may be far more detrimental to financial futures than once thought, particularly for those with the highest levels of debt: students of color and students from low-income families.” The data used was of 2008 bachelor’s degree recipients.

The Consumer Financial Protection Bureau has reported that the share of young consumers among first-time homebuyers is falling. According to the National Association of Realtors, Americans between the ages of 25 and 34 made up 27 percent of all homebuyers in 2011, the lowest share in the past decade. That percentage represe nts a 25 percent decline year-over-year from 2010.

nts a 25 percent decline year-over-year from 2010.

Young borrowers with student debt are less likely to own a home than those with no debt. According to recent analysis by the Federal Reserve Bank of New York, young borrowers with student debt - historically an indicator of a college education and an accompanying boost in wages - demonstrate a lower rate of homeownership than their peers with no student debt, breaking a decade-long trend.

The demos report found that family income has a large impact on the debt levels of college graduates. Seventy-five percent of bachelor’s degree recipients from families with incomes of less than $60,000 graduated with some student loan debt in 2008, compared to just 48% of students whose families earned $100,000 or more. Students from poorer families were also much more likely to graduate with large amounts of debt: 14% of graduates from lower-income families had more than $30,500 in debt, compared to just 9% of students from families who earned $100,000 or more.

A report by the Project on Student Debt in October 2012, an initiative of the Institute for College Access & Success, indicated that Connecticut students graduating in the class of 2011 had the fifth highest average student loan debt in the nation, at $28,783. That report also indicated that “high debt states are mainly in the Northeast and Midwest, with low debt states mainly in the West and South.” The report found that 64 percent of graduating students in 2011 had student debt, which ranked Connecticut 15th in the nation that year.

Earlier this year, the Consumer Financial Protection Bureau indicated that 1 in 5 U.S. households have student loans, and the number of student loan borrowers increased 31 percent between 2007 and 2012. Demos predicting that the “impact on the lifetime assets of indebted households will be nearly four times the amount borrowed.”